|

|

|

|

|

|

.jpg)

MarketMinute | What's the highest median existing home price ever?

|

|

|

- Inflation and higher mortgage rates are taking their toll on the nation’s homebuilders. Builder confidence fell for the 4th straight month in April.

- Housing starts rose unexpectedly in March, increasing 0.3%. However, starts for single-family housing tumbled amid rising mortgage rates.

- The median price of an existing home sold in March was $375,300, a 15% year-over-year increase and the highest median price ever recorded.

Green mortgages do exist, but what exactly are they? Green mortgages are an environmentally friendly type of home loan. How do you make a mortgage environmentally friendly; you might ask? Green mortgages, also known as Energy Efficient Mortgages (EEM), are a special type of loan designed to make your home more energy efficient while saving you money at the same time. Interesting, right?

How Do Green Mortgages Work?

These loans help you borrow money to pay for energy efficient upgrades to your home. The cost can be added into the mortgage or rolled into your current mortgage through an energy efficient refinance to allow you to make improvements to your current home. It’s an affordable way to make upgrades that may be costly up front, but in the long run will save you money.

What Can You Use Energy Efficient Mortgages Towards?

Whether you're a homeowner looking to improve your current home or are shopping for a home to purchase, you can use an EEM to make energy-efficient improvements. Changes you make to your home can improve energy efficiency and lower heating/cooling costs. An important bonus: These improvements can add to the value of your home.

- Installing Double-pane windows

- Replacing outdated air ducks

- Replacing old insulation

- Tankless water heaters

- High Efficiency Furnace or Air Condition System

Can a Green Mortgage Reduce Your Home’s Carbon Footprint?

According to the Center for Climate and Energy Solutions, the average U.S. family can spend $2,000 a year on energy bills, which means reducing your home energy use is the single most effective way to save money and reduce your home’s contribution to climate change. In fact, here are some interesting statistics to think about:

-

You can save 10% on energy costs by insulating, sealing, and weather-stripping the cracks around your windows and doors.

-

By sealing and insulating the ducts in your heating system, you can improve efficiency by as much as 20%.

-

According to the Department of Energy, energy loss from outdated windows accounts for nearly 25% of the annual heating and cooling costs for the average American home.

-

New energy-efficient heating or cooling equipment can cut your energy use by 20% or more.

-

The Environmental Protection Agency reports that you could save roughly $180 a year by using a programmable thermostat.

Overall, EEM’s allow families to save money, help the environment and help you to live more comfortably. Energy efficient homes tend to be cooler in the summer and warmer in the winter, cost less to maintain and have lower utility costs.

What Types of Green Mortgages does Greenway Offer?

Greenway Mortgage is proud to introduce our Green Mortgage Program that helps homeowners add energy efficient features to their home. Take a look below at the two types of EEM’s we offer:

FHA Energy Efficient Mortgage

This type of EEM provides additional financing that equals the lesser of 5% of the home’s appraised value, 115% of the median area price of a single-family dwelling, or 150% of the national conforming mortgage limit in the area. Click here to view the current FHA Loan Limits.

Contact Greenway Mortgage for more information and to see if you qualify.

VA Energy Efficient Mortgage

Military members, veterans, and their families who want to go green in their homes can do so with a VA Energy Efficient Mortgage. If the borrower is planning on making energy-efficient upgrades in the home, they have six months following the closing of their loan to complete those projects. If the borrower hopes to purchase a home that is already energy-efficient, the lender may increase the loan by as much as $6,000, so long as it meets specific energy-efficient standards.

Who Is an EMM Designed For & What Are Some Benefits?

-

Anyone can qualify for an energy efficient mortgage. However, the lender must validate that your home is an energy efficient property or that the improvement projects you want to pursue to make it an energy-efficient property are cost-effective.

-

An EEM can benefit those who hope to make a competitive offer on a house. Not only will the financing fund the energy efficient upgrades, but it can increase their offer price to beat out other buyers.

-

If you’re someone who intends to own your home for many years, EMMs make sense as you’ll be able to reap the savings benefits.

-

If you want to increase the value of your home energy-efficient upgrades are key. Some home buyers will pay more for a house with green updated features.

-

If you’re a homeowner with an energy-efficient home, you may be eligible for tax credits and rebates. Consult with your tax advisor for more information.

Bottom Line

If energy efficiency is important to you, a Green Mortgage may be something to think about as it reaps many homeowner benefits. For more information and to see if you quality for our Green Mortgage Program reach out to the experts at Greenway Mortgage.

.png)

3 Tips for Single Home Buyers: How to Make Your Dream of Homeownership A Reality

The thought of buying a home on your own as a single home buyer can be intimidating. If you’re making this leap, it’s going to take careful planning and the right team of experts.

Research from Freddie Mac shows 28% of all households (36.1 million) are sole-person, and that number is growing. Over the past 40 years, the number of sole-person households has nearly doubled, and that’s a trend that’s expected to continue as more and more Americans choose to live alone.

“Our calculation suggests that there will be an additional 5 million sole-person households in the United States by the next decade. This means 42% of the household growth will be contributed by sole-person households, . . .”

Do you fall into this category? Here are three tips to help you achieve your homeownership goals.

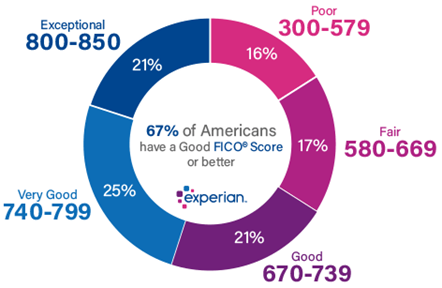

#1 Know Your Credit Score

When you buy a home on your own, you must qualify for your loan based entirely on your finances and credit history. Mortgage lenders will look at your credit profile only so it’s a good idea to review your credit report in advance.

Answer this question here to help you better understand where you may currently stand.

Do you have established credit?

Yes: Great! Keep making those payments on time. Avoid applying for more credit as it will lower your credit score. Every point counts!

No: Start building your credit now. A credit card or secure loan is a great option. But the length of history is important followed by the amounts you owe.

Find out what your score is and see where it falls. If you’re not sure if it’s strong enough or where to focus your energy to improve it, meet with a professional for expert advice on your situation.

#2 Explore Down Payment Options

Your next option is to investigate down payment mortgage programs so you can get a feel for what you’ll need to save to buy a home. Greenway Mortgage offers a variety of down payment programs and first-time homebuyer programs. We’ll see which program best suits your personal needs.

Check Out Some Of Our Programs Here:

#3 Think About Your Future Home and Your Needs

What is it that you want in a home? Here are some questions to ask yourself:

- What type of home do you picture yourself living in?

- What are your wants and needs in a home?

- How many bedrooms and bathrooms do you want?

- Do you need extra space for a home gym, a home office, or for entertaining>?

- Do you want to live in a detached home, a condo, or a townhouse?

While buying a home solo can feel like a big challenge, it doesn’t have to be. If you lean on the professionals, they can help you navigate these waters and make sure you’re able to take advantage of the great opportunities in today’s housing market (like low mortgage rates) to buy your dream home.

Bottom Line

The share of sole-person households is growing. If you’re looking to buy a home on your own, be confident that the dream is achievable. When you’re ready to begin your search, work with the experts at Greenway Mortgage so you have advice each step of the way.

Helpful Home Buying Resources

Check out some of our home buying resources here:

MarketMinute | How does current inventory compare to 2020?

|

|

|

|

|

|