Fed Increases Rates This November

Let's look beyond the Fed rate increase. As expected, the Fed raised policy rates by 0.75% at their November meeting. That's not the most interesting thing.

Investors were hoping the Fed would signal it's ready to ease off the current pace of rate hikes. And that's what happened. The Fed's statement hinted the Committee may pull back to allow time for the economy to feel the impacts of changes, though it's still committed to using rate increases to tame inflation.

As usual, there's no need to assume mortgage rates will rise the same amount as the Fed's rate boost. Other market forces are also at play, and rates often move before the Fed acts, in anticipation of their changes.

What should you do if you want to purchase or access cash from equity?

If this is your time to make a home financing move, don't let rates stop you.

In some areas, bidding wars have stopped, sellers have adjusted their prices and buyers are back in control. The payment to make an acceptable offer on the home you want may not be much different than if you had to pay over asking prices before.

Let's find a way to work within the framework of the current environment. Options like hybrid ARMs, buydowns and HELOCS can help.

Background on the Fed:

-

The Federal Reserve Board (the Fed) controls the federal funds rate and discount rate, which are charges for overnight loans from bank to bank or from the Fed to member banks.

-

The rate was lowered to near zero in March 2020 in response to the pandemic. These historic measures are now being reversed.

-

This is the sixth increase this year.

Don't let interest rates hold you back from making a move or accessing cash. The team at Greenway Mortgage is happy to help you navigate this market. We're still closing loans every day! Reach out if you have any questions.

.png)

|

|

|

|

|

|

.jpg)

|

|

|

|

|

|

When interest rates were at historic lows, a typical fixed rate mortgage loan was all most people needed. Now, rates have risen. They’re still below long-term averages, yet appreciably higher than before. And of course, higher interest rates lead to higher monthly payments.

Here at Greenway Mortgage, we recognize the rising rate environment and how homeownership may feel out of reach for some. That’s why we now offer a 2-1 Buydown Program to help counteract the trend towards higher rates.

It’s what everyone’s talking about these days, a 2-1 Buydown. We’re sure you’ve probably heard of it, but you may not know exactly what it means. That’s where we come in.

What is a 2-1 Buydown Loan?

With a 2/1 Buydown, borrowers get a 30-year fixed rate loan with an interest rate that’s temporarily discounted 2% during the first year and 1% the second year by paying an upfront fee at closing. By the third year of the mortgage term, the interest rate reaches the original interest rate on the loan.

Borrowers can ease their way into a home with lower payments that simply step up at the end of the first and second year then remain fixed for the remainder of the loan. Here are the details:

Program Details:

- 1st Year: Interest rate starts at 2% under the locked rate

- 2nd Year: Interest rate is 1% below the locked rate.

- 3rd Year: Loan converts to the locked interest rate.

The Fine Print

- Borrower must qualify for full monthly payment (before buydown rate is applied).

- Third-party contributions are eligible.

- Eligibility requirements, exclusions and other terms and conditions apply.

Example of a 2-1 Buydown

Say you lock in a 5% interest rate, the 2-1 Buydown Program allows you to make monthly payments at a 3% interest rate for the entire first year of your mortgage.

Then, in year two, your payments would be based on a 4% interest rate.

Finally, once you hit year three and for the remaining life of your loan, your payments would reflect your originally-agreed-upon 5% interest rate.

What Types of Loans is a 2-1 Buydown Available For?

2-1 Buydowns are available on conforming fixed products.

- 30-year Fixed Rate Conforming Loans*

- Conventional Purchases | Primary: 1-4 Units, Second Home: 1 Unit

- Conventional Refis | Limited Cash-out

- HomeReady / HomePossible | Purchase Primary: 1 Unit

- FHA, VA, USDA | Purchase Primary: 1-4 Units

- FHA 2nd Home | 1 Unit

*High Balance available Conventional, HomeReady, HomePossible

Who Can Benefit From a 2-1 Buydown?

- Borrowers who may earn more within a few years of obtaining mortgage.

- Borrowers who want to use the savings to reduce bills/debt.

- Borrowers receiving contribution or gifts that will fund the buydown at closing.

How Can a Borrower Benefit from a Temporary Buydown?

- Borrowers will pay less money upfront on their monthly mortgage payments.

- It helps ease borrowers into making monthly payments and it saves you money during the first two years of homeownership.

- Lessens the burned on your wallet with any extra expenses typically associated with moving into a new house (furniture, paint, new appliances, etc.)

Why are we seeing the 2-1 Buydown Program now?

In an environment where interest rates are rising, the 2-1 buydown benefits home buyers by helping them ease into the full monthly payment. It’s especially appealing for first-time homebuyers who are having a hard time purchasing a home in a housing market like we’re seeing today.

Bottom Line

If you’re currently house hunting in this turbulent housing market and need to find solutions to lower your monthly payments, this is a program is worth exploring. The market is shifting, but while it’s influenced by high interest rates and high home prices, borrowers may benefit from a 2-1 buydown.

So, are you interested in purchasing a new home and like the idea of easing into your mortgage payments? Contact the team at Greenway Mortgage to get started.

.png)

3 Biggest Questions About Real Estate and Mortgages

As we near the end of 2022, the housing market is still in a constant state of shifts and changes. Some bigger or more impactful than others, but the truth remains the same: while we wish we had a crystal ball, we’ll never be able to predict what’s going to happen. However, one thing will always remain constant: people will always need a place to call home.

There are three big questions in real estate and in the mortgage industry right now. We’ll cover them here. So, before you hit the panic button, give this a read!

Will Mortgage Rates Continue to Rise?

To answer this question, it’s important to understand the why behind the reason mortgage rates have doubled since the beginning of the year and that’s due to inflation.

To ease inflation, the Federal Reserve is taking steps to tame inflation by slowing the economy. In turn, these decisions have an impact on mortgage rates. Until this is under control, we may continue to see rates stay high or rise even higher.

Despite the high mortgage rates, there is still opportunity in the real estate market.

“There is no doubt that the increasing mortgage rate will make homebuying even more challenging, . . . buyers may still find opportunities, as these changes coincide with the time of the year when buyers have historically found the best market conditions to obtain more bargaining power,” said Jiayi Xiu, economist for realtor.com.

What Will Happen to Home Prices?

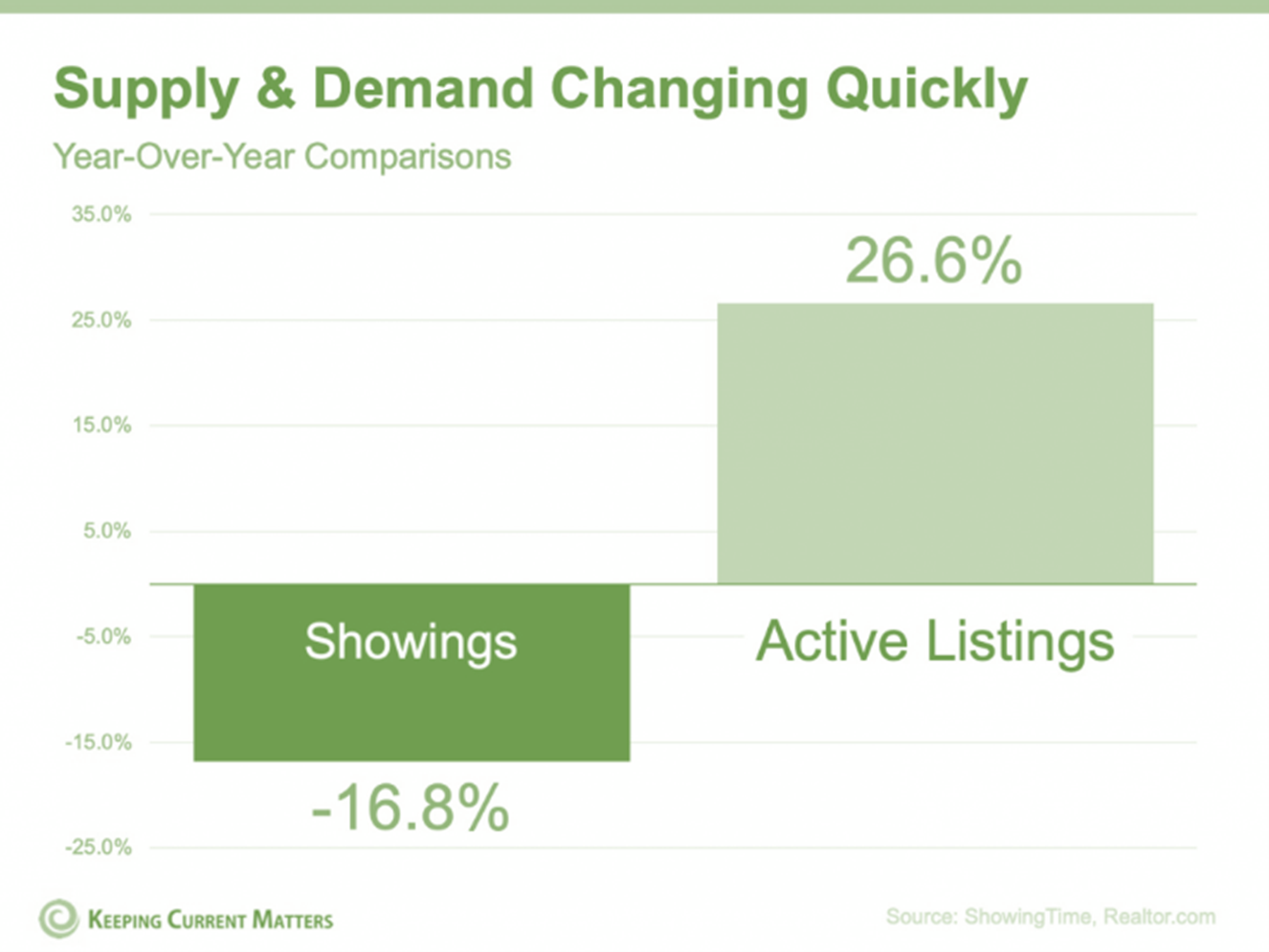

Dave Ramsey sums it up: “The root issue of what drives house prices almost always is supply and demand.”

And when you look at the graph below, you’ll see why we have seen such a large slowdown in home price appreciation in the last few months.

The sudden uptick in mortgage rates and lingering inflation has changed the playing field in the housing market. So, as the pace of sales slows, the more active listings there are. That does not mean we’ll see national deprecation in home values.

Overall, experts are projecting continued price appreciation in most markets, averaging about 1.8% in 2023. However, there are some overheated areas where experts are projecting slight depreciation, but certainly not enough to call it a crash.

Should I Buy A Home Right Now?

Homeownership has many financial and non-financial benefits. It’s true that it costs more to buy a home today than it did last year, but the same is also true for renting. This means, either way, you’re going to be paying more.

Although affordability is challenging right now, buying a home helps you gain equity will will help grow your net worth.

The best way to answer this question is that homeownership will always win over time. It’s a long game.

You can choose to put your money over time into rent and not get a return or play the long game, invest in homeownership and benefit from your investment.

Bottom Line:

As we said before, we wish we had a crystal ball to predict what’s going to happen with mortgage rates or price appreciation, but we unfortunately can’t control that.

Remember, the team at Greenway Mortgage is always here to help answer any questions you have. We are happy to sit down with you to discus which home buying option best suites your scenario and find out how much home you can afford. We’re here to help.

Here are some helpful resources:

- Loan Products

- First Time Home Buyer Resources

- Mortgage Calculators

- Get Pre-Approved

- Apply Now

- Contact Erin The Expert

.png)